If you are looking at your commercial card portfolio, you are looking at a math problem with a very expensive leak. Banks are currently losing an estimated $50 billion per year in interchange revenue to fintech businesses.

The common assumption is that these customers are leaving for better rewards or flashier marketing. But when you look at the data, the real driver is much simpler: the path of least resistance. Your customers aren’t choosing cards based on a 0.1% difference in cash back; they are choosing the card that saves their finance team from a 40-hour-a-month headache.

At Sage Expense Management (SEM), we’ve tracked the impact of moving from a plain plastic card to a “smart” one. The results are consistent: when a card is paired with real-time text-to-receipt automation, spend volume jumps by an average of 160% to 169%.

The Psychology of the “Top of Wallet” Card

Think about the last time an employee at one of your commercial clients went to buy gas or office supplies. They probably have two or three cards in their wallet—yours, their personal card, and maybe a fintech card like Ramp or Brex they signed up for because the software looked cool.

If using your card means they have to save a paper receipt, remember to upload it to a clunky portal three weeks later, and then follow up to all the “nagging” emails from their bookkeeper, they are going to stop pulling your card out.

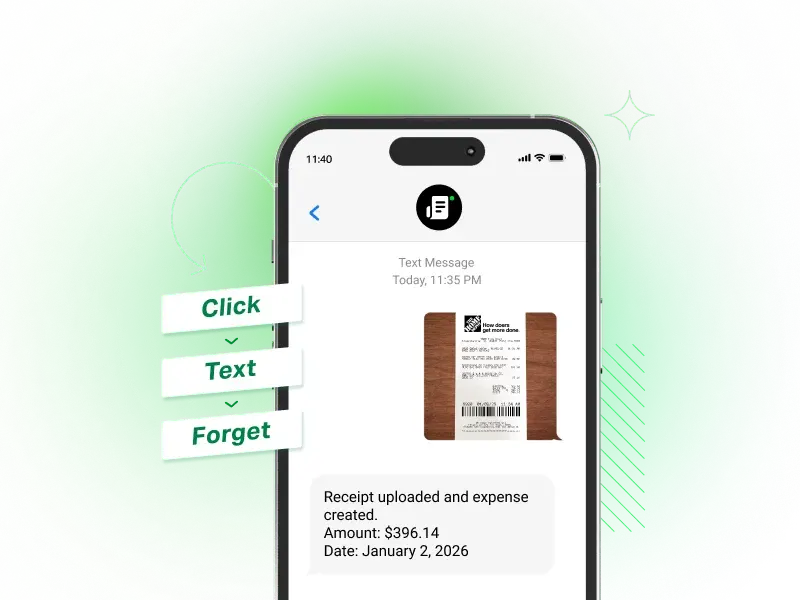

However, if that card is connected to a real-time feed, the experience changes completely. The second they swipe, they get a text: “You have a new expense of $X. Please reply with a photo of the receipt and we will match it”. They snap a picture, hit send, and they are done before they even put the truck in gear. By making your card the easiest one to use, it naturally becomes the “top of wallet” choice for every single transaction.

Turning Documentation into Revenue

The ROI of a text-to-receipt feature isn’t just about “convenience”—it’s a direct revenue driver for the bank. In our experience, 85.87% of employees using SEM submit their receipts within the first 24 hours.

This immediate capture does two things for the bank’s bottom line:

-

Recaptures leaked volume: Every dollar your client spends on a fintech card is a fee your bank loses. By providing a “smart” experience on your existing cards, you pull that leaked volume back into your ecosystem.

-

Drives “text-first” compliance: In our experience, 65% of employees submit their receipts within the first 30 minutes of spend when nudged via text. This eliminates the end-of-month reconciliation “crunch” that causes finance teams to churn.

-

Solves the “silent churn”: You stop the slow bleed of deposits. When a client’s daily operational spend stays on your card, you maintain the visibility you need to keep that primary operating relationship secure.

Saving the Finance Team (and the Relationship)

In most SMBs, the finance team is exhausted. They spend their lives playing private investigator—trying to figure out why someone spent $400 at a hardware store three weeks ago. This friction is what eventually drives them to look for a “better” solution outside of their bank.

When you embed Sage Expense Management, you aren’t just giving them an app; you are giving them an automated expense management partner ready to take the load off the finance team. The system takes over the time-consuming work of gathering receipts and matching them to transactions, so the finance team doesn’t have to spend their time chasing people down.

For the bank, this means your Relationship Managers aren’t getting pulled into low-value troubleshooting or apologies for clunky tech. Instead, they are free to focus on growing the relationship.

Real Growth in under 4 Months

The most compelling part of this ROI analysis is the speed of implementation. You don’t have to wait for your legacy processor like FIS or Fiserv to update their 2026 roadmap.

Because Sage Expense Management (formerly Fyle) is card-agnostic and has zero technical dependency on your core banking tech, you can launch this “smart” experience to your customers in under 4 months.

You already are issuing the cards and you already have the trust. By adding the “smart” software layer, you turn a commodity product into a revenue-generating engine for your commercial portfolio.